The stock of MicroStrategy declined to more than $300 in the after-hours session on Dec. 30. Could MicroStrategy be slowly losing its heat?

The MicroStrategy stock (MSTR) is down by 46% from its all-time high in November. This comes as the company’s bid to increase its stock shares by billions of dollars in order to back its funding strategy of $42 billion.

According to Google Finance statistics, the firm’s shares fell for the second consecutive day, and the price level reached a whopping low of $ 302.96, meaning a loss of 8.2 % in the stock value. Late-hour trading resulted in a further decrease of the stock price by three percent to $293.59.

Last week, MSTR acquired 2138 BTC, which increased the total amount to 446400 BTC. Additionally, its shares were added to the index of Nasdaq 100 on Dec. 23, after which its shares surged by 402%.

However, ever since the intraday high was reached on Nov. 21 at $543, MSTR has been on the downslide. This fact, however, does not take away the focus from the fact that the firm reported 342% growth for the year so far due to the aggressive accumulation strategy of Bitcoin (BTC) that MSTR has been undertaking alongside the gained high price surge of 121% of the cryptocurrency.

Is MicroStrategy losing its momentum?

MSTR’s BTC amassing approach has been challenged by Martin Shkreli, who co-founded the hedge funds Elea Capital. He called Michael Saylor an “overzealous” and “not credible” supporter of BTC. “The worst vote I’ve ever seen in the history of proxy voting,” he said, referring to MSTR’s shareholder vote on Bitcoin treasury allocation that garnered just 0.5% support on Dec. 24. Shkreli said that market sentiment has changed and that it is now “a little bit hard to see the bull case” for the price of BTC, implying that Saylor’s aggressive multibillion-dollar purchases had underperformed.

This is not the first time the company has faced criticism. Some analysts, including Kobbeissi Letter and Jacob King, believe that MicroStrategy operates like a Ponzi scheme because it relies very heavily on debt and equity issuance to buy BTC, which dilutes shareholder value.

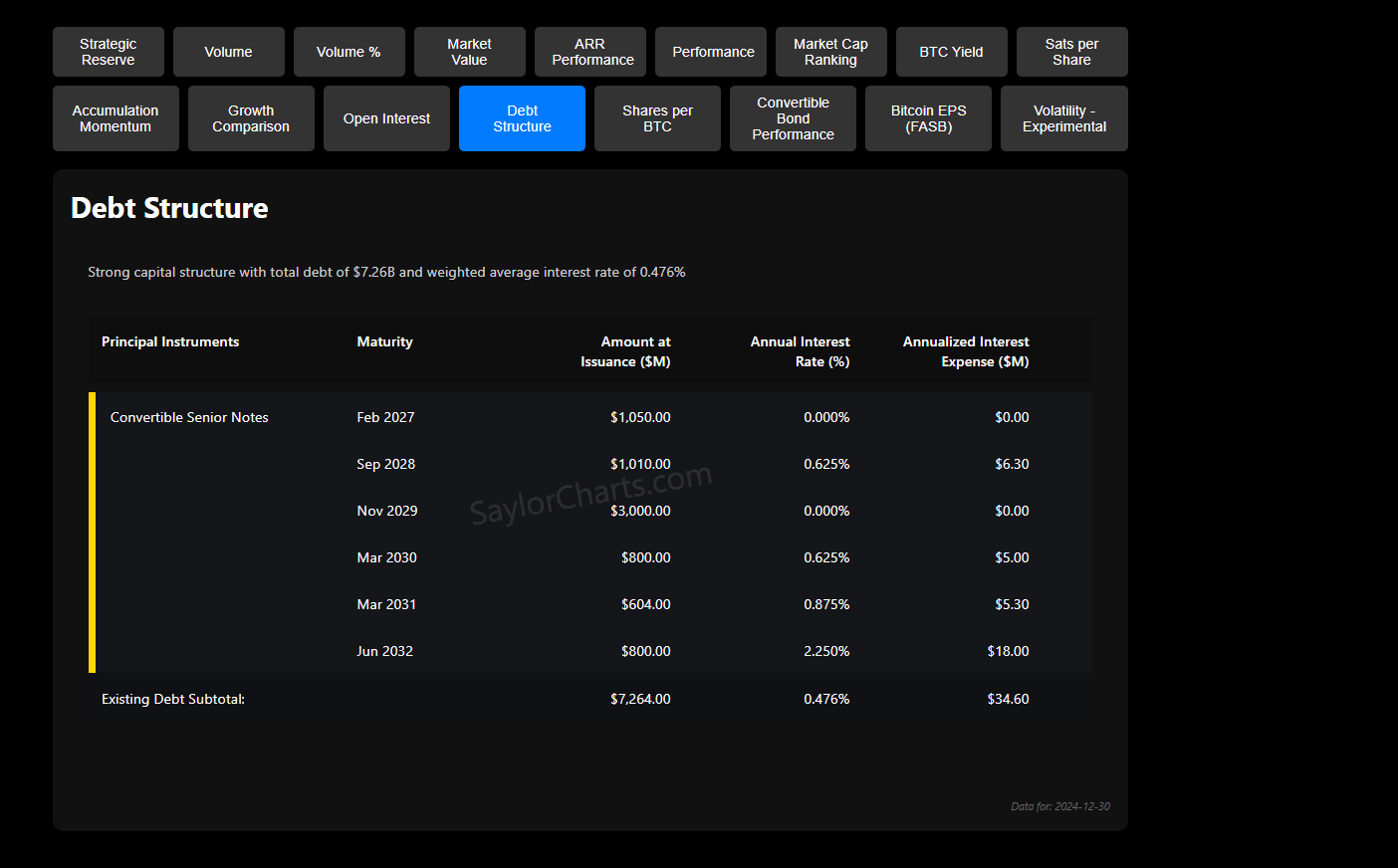

Felix Hartmann of Hartmann Capital is more optimistic, arguing that the near-zero interest rates and maturities spaced out between 2027 and 2030 make MicroStrategy’s short-term debt commitment manageable. Hartmann said, “Every BTC dip brings doomsayers; every pump resets the MSTR premium and makes Saylor look like a genius,” anticipating that MSTR will surpass five in market value before collapsing. There is disagreement among investors on how the shareholder vote will steer MSTR toward its ambitious ‘Bitcoin 21/21’ goal as the firm enters its next phase.

This article first appeared at crypto.news